Application Areas

Control Numerical Evaluation

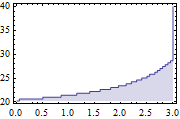

Compute the critical value surface of an American put option using a custom number of grid points.

| In[1]:= |  X |

| Out[1]= |  |

| New in Wolfram Mathematica 8: Built-in Financial Computations | ◄ previous | next ► |

| In[1]:= | X |

| Out[1]= | |