Perform Autoregressive Filtering

Filter data using an autoregressive Kalman filter.

| In[1]:= | X |

Fit an autoregressive model to the data using EstimatedProcess.

| In[2]:= | X |

| Out[2]= |

Filter the data according to the estimated process using KalmanFilter.

| In[3]:= | X |

| Out[3]= |

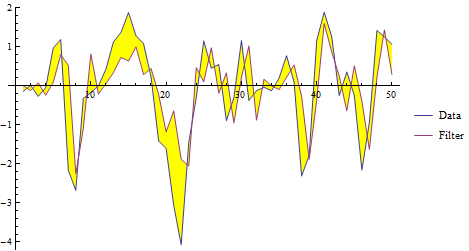

Compare the data and the filter.

| In[4]:= |  X |

| Out[4]= |  |