Extended Hypothesis Tests for Dispersion Equivalence

BrownForsytheTest, ConoverTest and LeveneTest have been extended to allow for testing the dispersion equivalence hypothesis with multiple samples.

Brown–Forsythe and Levene tests assume that data is normally distributed, while the Conover test has more relaxed conditions and only assumes that datasets are symmetric about a common median.

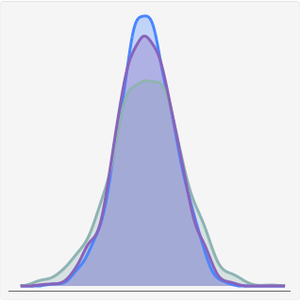

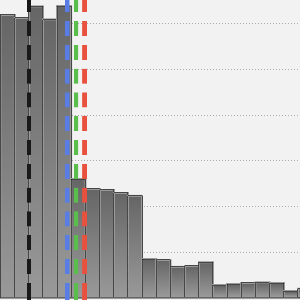

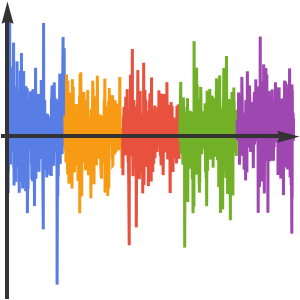

Compare the variance of daily point changes in the S&P 500 for a few years.

Create yearly time series.

Compute daily differences for each yearly time series.

Asses if the difference time series are normally distributed.

Since not all of the samples are normally distributed, many variance tests are not applicable. Check the assumptions of the Conover test.

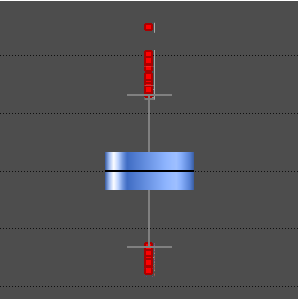

You can assume that each time series is symmetric about 0: the preceding plots show symmetry around 0 and the medians are close enough to 0.

Use the Conover test to assess if all the time series have equal variance.

You can conclude that the variance of daily point changes is not the same for each of the observed periods.