Identify Conditional Heteroscedacity

TimeSeriesModelFit automatically checks for conditional heteroscedacity in data and fits ARCH/GARCH models to data.

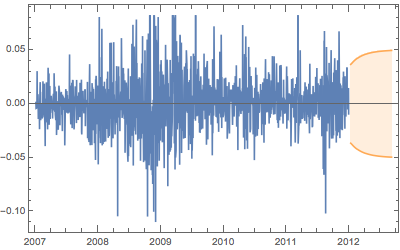

Create a time series of daily returns on Starbucks Corp. stock.

show complete Wolfram Language inputhide input

| Out[3]= |  |

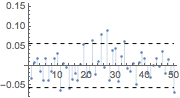

Compute the autocorrelation function.

show complete Wolfram Language inputhide input

| Out[5]= |  |

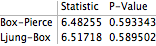

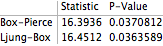

Test for autocorrelation in the sequence of returns.

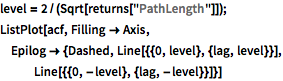

| Out[6]= |  |

The returned time series is not autocorrelated, but its square is.

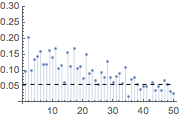

| Out[8]= |  |

| Out[9]= |  |

TimeSeriesModelFit determines the GARCH family as the best fit for the data.

| Out[10]= |  |

Find the fitted process.

| Out[11]= |  |

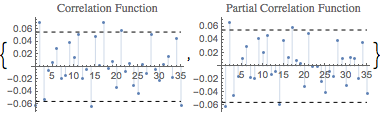

The model residuals appear uncorrelated.

| Out[12]= |  |

| Out[13]= |  |

Use TimeSeriesModel to compute confidence intervals of future forecast.

| Out[15]= |  |