Estimation of Irregularly Sampled Random Processes

Generate a realization of an irregularly sampled OrnsteinUhlenbeckProcess.

In[1]:=

sample = TimeSeriesResample[

RandomFunction[

OrnsteinUhlenbeckProcess[0, .1, .3], {0, 100, .1}], {Sort[

RandomReal[100, 1000]]}]Out[1]=

show complete Wolfram Language input

Out[2]=

Estimate the process parameters from irregularly sampled data.

In[3]:=

EstimatedProcess[sample,

OrnsteinUhlenbeckProcess[\[Mu], \[Sigma], \[Theta]]]Out[3]=

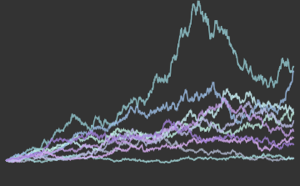

Retrieve the stock prices for GE since January 1, 2013, and convert them to TemporalData .

In[4]:=

price = TemporalData[FinancialData["GE", "Jan. 1, 2013"]]Out[4]=

show complete Wolfram Language input

Out[5]=

The time stamp of the stock price data is nonuniform.

In[6]:=

MinMax[Differences[price["Times"]]]Out[6]=

Assume the log price satisfies FractionalBrownianMotionProcess and estimate the parameters.

In[7]:=

EstimatedProcess[Log[price],

FractionalBrownianMotionProcess[\[Mu], \[Sigma], h]]Out[7]=