Apply ARMA Filter to a Heavy-Tailed White Noise Process

Sample the process of independent and identically distributed random variables from Student  distribution.

distribution.

| In[1]:= | X |

| Out[1]= |

Apply ARMA filter to the white noise signal.

| In[2]:= | X |

| In[3]:= | X |

| Out[3]= |

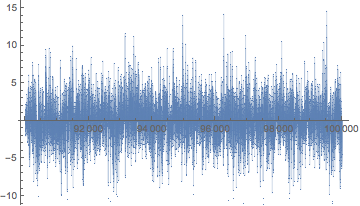

Extract the tail of the path, where the sequence has settled into stationary regime.

| In[4]:= | X |

| In[5]:= | X |

| Out[5]= |  |

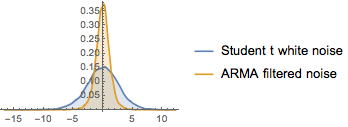

Compare slice distributions of the unfiltered and the filtered signals.

| In[6]:= | X |

| In[7]:= |  X |

| Out[7]= |  |