Test for Serial Correlation

Generate random sample of an ARProcess.

| In[1]:= | X |

The estimated correlation function slowly decreases as a function of lag.

| In[2]:= | X |

| Out[2]= |  |

Test for serial correlation up to lag 10.

| In[3]:= | X |

| Out[3]= |  |

The tests confirm that data is serially correlated.

| In[4]:= | X |

| Out[4]= |  |

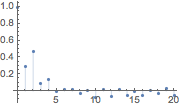

Now generate a random sample from a GARCHProcess.

| In[5]:= |  X |

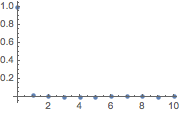

The values of the estimated correlation function at nonzero lags are very small.

| In[6]:= | X |

| Out[6]= |  |

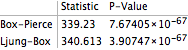

Check the first path with the AutocorrelationTest.

| In[7]:= | X |

| Out[7]= |

| In[8]:= | X |

| Out[8]= |  |

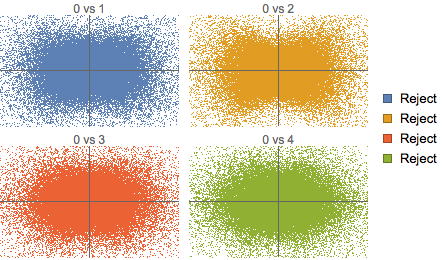

There is no serial correlation, but the slices are not independent.

| In[9]:= | X |

| In[10]:= | X |

Check the independence between the slice at time zero and the four following slices using Hoeffding's independence test.

| In[11]:= |  X |

Show scattered plots of slice values at time zero and at other times and the conclusions of the test.

| Out[12]= |  |