Model Option Prices Using Merton Jump-Diffusion

Define Merton's jump-diffusion model for option pricing.

| In[1]:= |  X |

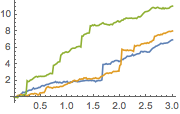

Simulate the process.

| In[2]:= |  X |

| In[3]:= | X |

| Out[3]= |  |

Compute slice properties for the process.

| In[4]:= | X |

| Out[4]= |

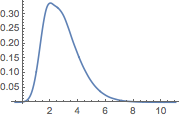

Approximate slice distribution from sample.

| In[5]:= |  X |

| In[6]:= | X |

| Out[6]= |  |